Beginner's Guide to Index Funds and Long-Term Investing

A simple, step-by-step primer on index funds: why fees matter, how diversification works, and how to build an automated, long-term investing plan.

Getting Started with Index Funds

Index funds are a straightforward way to invest in the broad market without picking individual stocks. At their core, index funds aim to match the performance of a specific market benchmark by holding the same securities in similar proportions. This simple, passive approach delivers instant diversification, spreading your money across many companies and sectors, which can reduce the impact of any single business underperforming. For beginners in personal finance, the appeal is clear: low maintenance, typically low expense ratios, and a transparent strategy. Index funds come as mutual funds or ETFs, both offering convenient access and easy portfolio building. While they do not guarantee profits and still experience volatility, they remove much of the guesswork associated with selecting winners. Instead of trying to beat the market, you participate in it, letting long-term market growth do the heavy lifting. This combination of simplicity, broad exposure, and cost control makes index funds a powerful foundation for building wealth over time.

How Index Funds Work

Index funds follow a rules-based methodology. They mirror a benchmark by holding the underlying securities, often using market-cap weighting, where larger companies have a bigger presence. Some funds use sampling to closely replicate performance without owning every component, which helps keep costs low. The difference between a fund's return and its index is called tracking error, and the driver of that gap is typically fees and operational frictions. ETFs trade throughout the day and use a creation/redemption mechanism that can enhance tax efficiency, while mutual funds transact at the end-of-day NAV and can offer features like automatic investments. Regardless of structure, the main goal remains consistent: capture the market's average result at minimal cost. Pay attention to the expense ratio, bid-ask spreads for ETFs, and how the fund handles rebalancing when the index changes. By understanding these mechanics, you can better evaluate which index fund fits your goals, risk tolerance, and trading preferences.

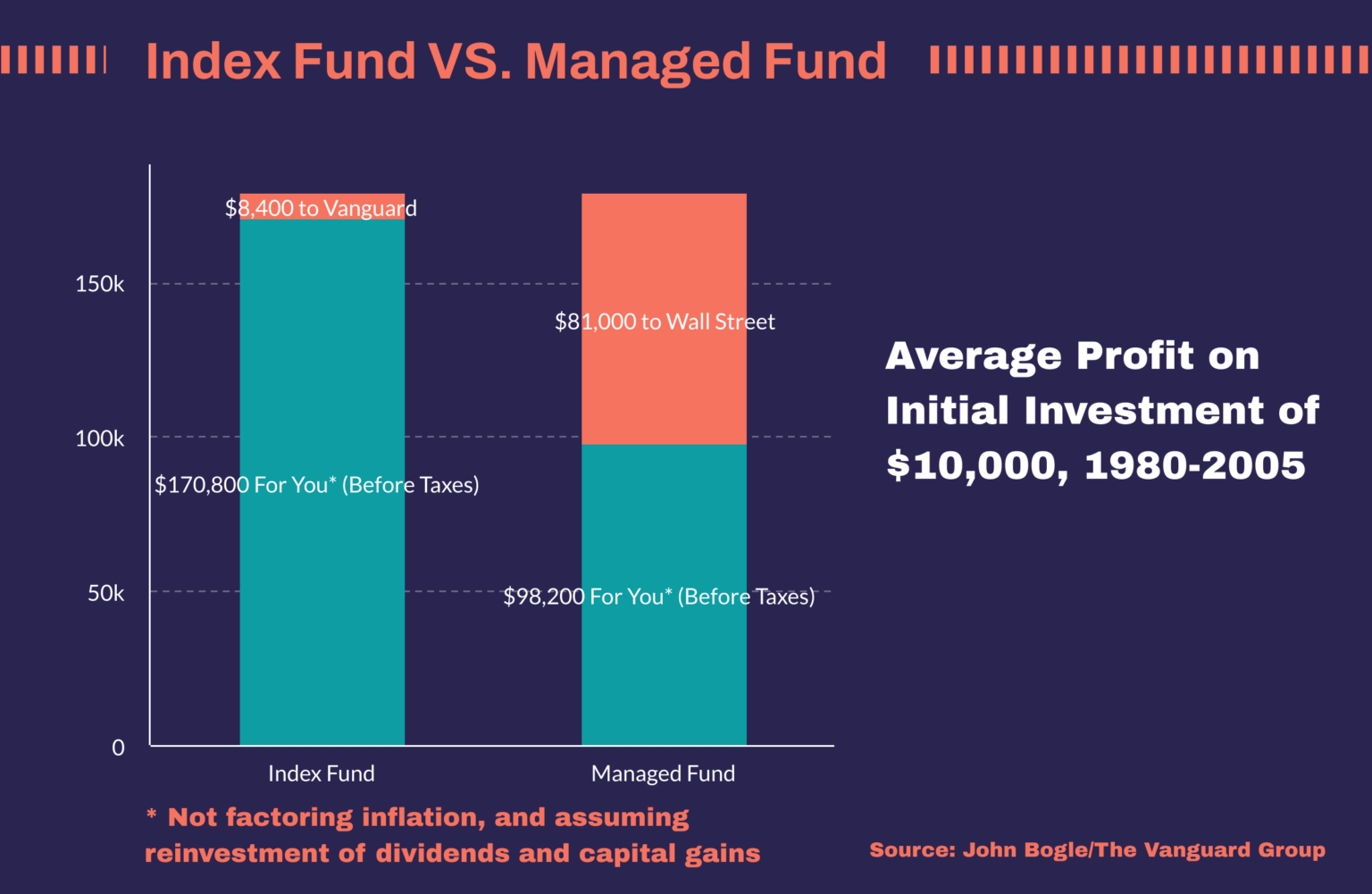

Why Long-Term Investing Wins

Successful investors focus on time in the market rather than short-term predictions. The power of compounding means returns earned on your investments can generate their own returns, a snowball effect that becomes more meaningful the longer you stay invested. Markets can be bumpy, and volatility is normal, but spreading investments across broad index funds helps smooth individual company risk while preserving potential growth. A long horizon can also reduce the emotional urge to time the market, a behavior that often leads to buying high and selling low. Staying invested through different market cycles gives you more chances to participate in rebounds after declines. Align your risk tolerance with your time horizon: longer-term goals can often support higher stock exposure, while shorter timelines may call for more conservative allocations. By combining diversification, patience, and disciplined contributions, long-term index investing turns unpredictable daily noise into a manageable path toward your financial objectives.

Building a Simple, Balanced Portfolio

A strong index-fund portfolio starts with asset allocation: the mix of stocks, bonds, and possibly other assets aligned to your goals and comfort with risk. Stock index funds target growth, while bond index funds offer stability and income, helping you stay invested during turbulence. You can keep it simple with a total stock index fund and a total bond index fund, or add international exposure for broader diversification. Implement dollar-cost averaging by investing a fixed amount at regular intervals; this approach reduces the pressure of perfect timing and builds consistency. Consider an automatic contribution plan to keep your strategy on track. Define rebalancing rules—either at a set interval or when allocations drift beyond a chosen band—to maintain your target mix without emotion. Keep a cash buffer for emergencies so you aren't forced to sell investments at unfavorable times. With clear goals, a sensible allocation, and systematic habits, your portfolio can grow steadily and resiliently.

Costs, Taxes, and Account Choices

Minimizing costs is one of the most reliable ways to boost net returns. Focus on low expense ratios, but also consider tracking difference, bid-ask spreads for ETFs, and any brokerage fees. For taxes, index funds are often tax efficient due to low turnover, which can reduce taxable distributions. ETFs typically have structural advantages that may further limit capital gains payouts, though mutual funds can still be efficient and convenient. Use tax-advantaged accounts for retirement goals to defer or reduce taxes, and consider asset location: holding less tax-efficient assets in sheltered accounts and more tax-efficient index funds in taxable accounts can improve after-tax outcomes. If applicable, strategies like tax-loss harvesting can help manage liabilities in taxable accounts, but ensure you understand rules and keep good records. The key is to evaluate investments on an after-fee, after-tax basis, matching account types and fund choices to your time horizon and personal financial plan.

Staying the Course Through Ups and Downs

Discipline is the backbone of long-term success. Create a simple investment policy statement that defines your goals, asset allocation, contribution schedule, and rebalancing plan. This written guide helps you resist performance chasing and panic selling during market swings. Expect downturns; they are a normal part of investing. Maintain your contribution plan, revisit your risk level only when your life circumstances change, and avoid frequent strategy shifts driven by headlines. Review your portfolio on a reasonable cadence, such as once or twice a year, to rebalance and confirm alignment with your objectives. Keep an emergency fund to prevent tapping investments at the wrong time. As goals near, gradually adjust toward a more conservative mix to protect what you've built. Remember, you control costs, behavior, and diversification—three levers that drive outcomes. By staying patient and methodical, index funds can help transform consistent habits into durable wealth over time.