Understanding Compound Interest: Let Time Grow Your Money

Learn how compound interest works, why starting early matters, and practical steps to maximize growth so your money works harder over time.

What Compound Interest Really Means

At its core, compound interest is growth on growth. Your money earns a return, and those earnings are added to your principal, so future returns are calculated on a larger base. Unlike simple interest, which pays only on the original amount, compounding treats each period's result as new seed for the next period. The compounding frequency—daily, monthly, quarterly, or annually—determines how often your balance gets updated, while APY captures the effect of compounding in a single percentage. Imagine placing 1,000 into an account at a steady rate: with simple interest you only collect the same fixed amount each period; with compounding, each credit slightly increases the next credit, creating a snowball effect. Over many periods, this produces exponential growth rather than a straight line. The principle is simple: keep money invested, reinvest earnings, and give compounding enough time to work.

Why Time Is Your Greatest Ally

Time is the quiet engine behind compound growth. A modest start, given a long time horizon, can outpace a larger start made later because the early dollars enjoy more rounds of growth-on-growth. Think of two savers: one deposits steadily and begins earlier, then stops; the other waits, contributes more for longer, yet still may fall short because the first saver captured more periods of compounding. This is the essence of exponential growth—small differences in start time create large differences in outcomes. The lesson is practical: prioritize starting, even with small amounts, and allow consistency to carry the load. Regular contributions amplify the effect, and reinvesting every distribution magnifies it further. Avoid chasing perfect timing; missing even a few strong growth periods can set you back. By focusing on time in the market, not timing the market, and letting earnings remain invested, you align your plan with the natural advantage that compound interest provides.

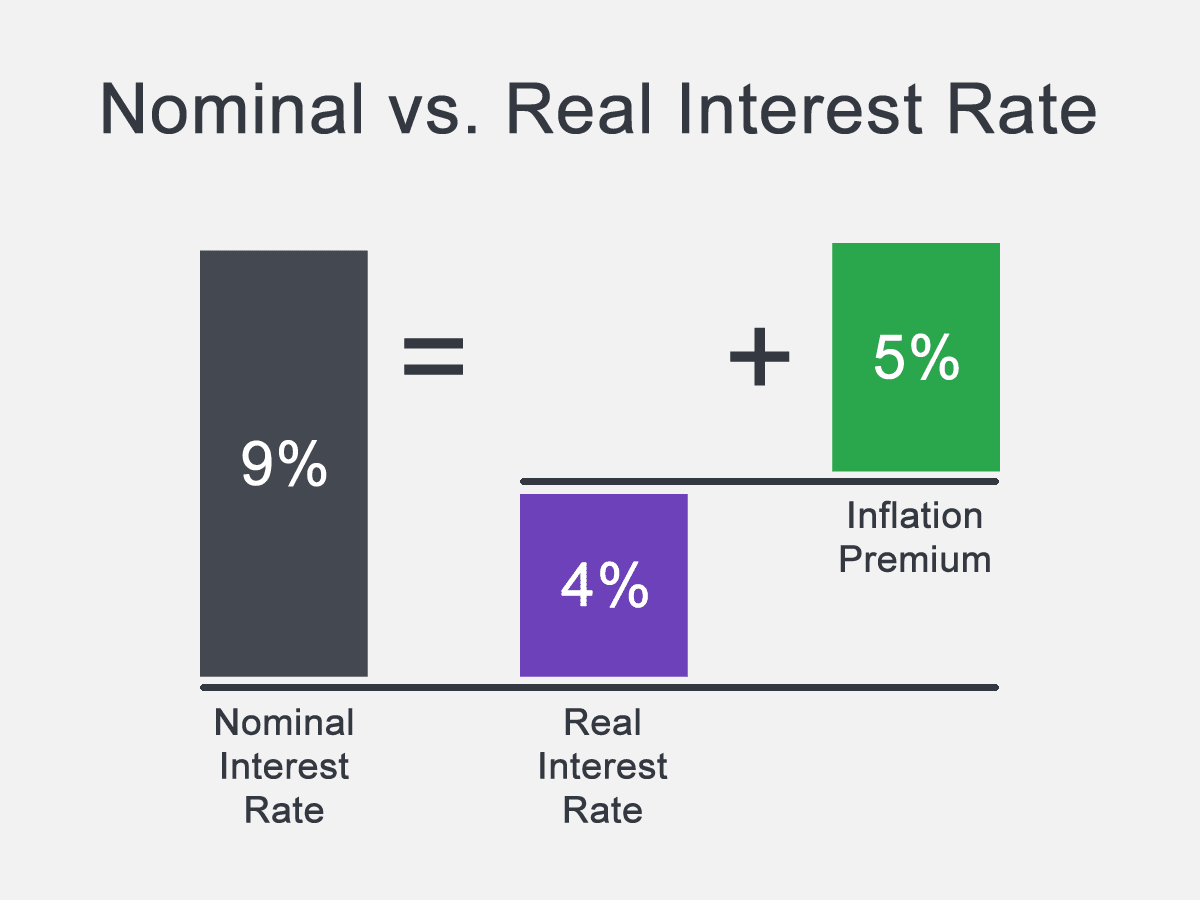

Rates, Frequency, and the APY Advantage

Two levers control compounding: your interest rate and your compounding frequency. The rate has the biggest impact; a higher rate accelerates the curve of exponential growth. Frequency matters too: more frequent compounding—such as monthly versus annually—adds incremental lift by updating your balance more often. The difference between APR and APY clarifies this: APR is the stated rate, while APY reflects the actual return after considering compounding. When comparing accounts or investments, focusing on APY gives you a fairer view of expected growth. That said, chasing slightly higher frequency yields diminishing returns compared with improving the rate or increasing contributions. Practical takeaway: prefer vehicles with competitive APY, reinvest all earnings, and avoid interruptions that reset your compounding clock. Over time, the combination of a solid rate, reliable frequency, and unwavering reinvestment can turn steady deposits into a substantial balance, even if each individual period's gain seems modest on its own.

Practical Ways to Harness Compounding

To make compound interest work for you, design habits that run on autopilot. Automate deposits so contributions happen before you can spend them, and practice dollar-cost averaging to add steadily through different market conditions. Reinvest dividends and interest so every payout becomes fresh principal. Consider modest, periodic increases to your contributions—raising by a small percentage when income rises can meaningfully accelerate results. Align your investments with a diversified, long-term mix that matches your risk tolerance, and rebalance periodically to keep your plan on track. Minimize fees, because every fraction taken out is a fraction that cannot compound. Use tax-advantaged accounts when available to reduce tax drag, preserving more growth. Maintain an emergency fund so you are not forced to interrupt compounding to handle surprise expenses. Most of all, stay consistent: many small, well-aimed decisions—made repeatedly—produce the powerful, cumulative effect that compounding is famous for.

Protecting Your Growth from Pitfalls

Compounding can work against you when it comes to high-interest debt, where charges accumulate on prior charges. Prioritize paying down expensive balances, because eliminating that negative compounding often delivers a higher, risk-free return than many investments. Guard your growth from fees, taxes, and inflation: keep costs low, use efficient accounts, and invest in assets with the potential to outpace rising prices. Avoid emotional decisions that break the compounding chain, such as panic selling after temporary declines. Build a resilient plan—sufficient cash reserves, proper insurance, and diversification—so you can stay invested through uncertainty. Review progress periodically, but resist the urge to tinker constantly. Embrace patience and discipline: these are the behaviors that let time do the heavy lifting. By minimizing drag, steering clear of costly debt, and committing to long-term habits, you protect the delicate mechanism of compound interest and allow it to transform consistent effort into lasting financial momentum.